One of the key features for Naya Pakistan is to improve the housing situation for Pakistanis. There is a shortfall of over 10 million houses, and every year we are adding to this backlog. This government intends to promote access to housing to the people of Pakistan and jumpstart the housing sector.

Download High Quality Naya Pakistan Housing Scheme Form NADRA

{kind=link}

How to apply

The people can avail the facility of online form and download it from the website of NADRA as the authority issued the document hours after Imran Khan’s inauguration of the project. While it can be submitted within two months (from October 22 to December 21) along with Rs250 registration fee at the selected district offices.

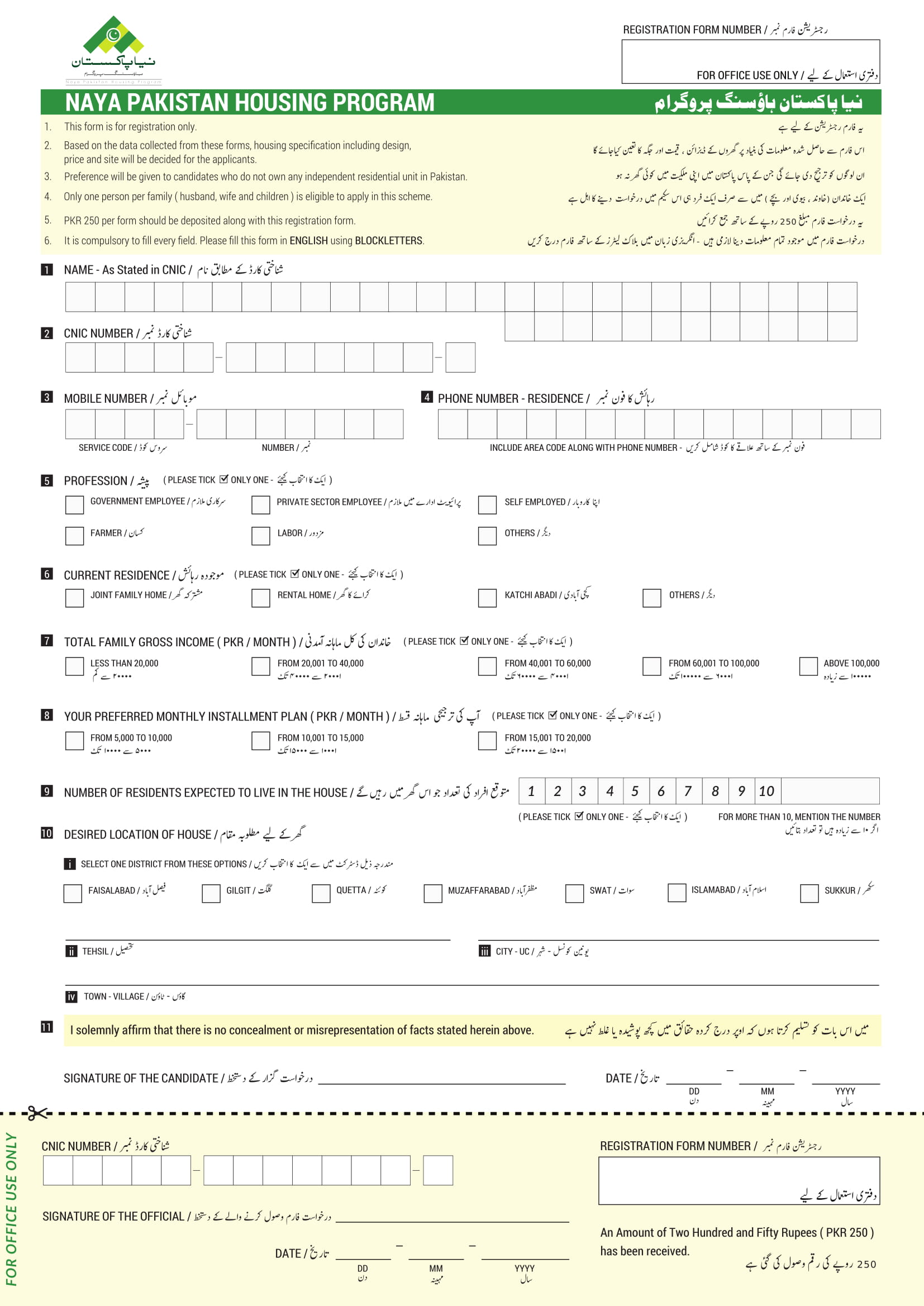

In the first phase of the project seven districts would be facilitated, including Sukkur, Quetta, Gilgit, Muzaffarabad, Swat, Islamabad and Faisalabad.

The eligibility criteria

Only one person per family (husband, wife and children ) is eligible to apply in this scheme.

Preference will be given to candidates who do not own any independent residential unit in Pakistan.

The homes are to be made for the common man, who earns Rs10,000-25,000 a month.

PKR 250 per form should be deposited along with this registration form.

Based on the data collected from these forms, housing specification including design, price and site will be decided for the applicants

Offices, where forms can be submitted:

SUKKUR: DC Office, Sukkur

QUETTA: NADRA Registration Center, adjacent Helper Eye Hospital, Sariab Road Quetta

GILGIT : DC Office, Gilgit

MUZAFFARABAD: DC Office old secretariat, Muzaffarabad

SWAT: DC Office, District Court, Mengura Swat

ISLAMABAD: NADRA Mega Center, Blue Area Islamabad

FAISALABAD: DC Office Faisalabad

The salient features of this housing is to make housing affordable to people are the following

- Increase buying power by providing loans of longer tenure fifteen to twenty years.

- Reduce cost by standardizing design and specifications.

- Reduce cost by significantly cutting down the approval time.

- Develop new communities with access to infrastructure.

- Reduce the upfront cost of builders by providing them land in installments and minimum time for approvals and infrastructure before start of construction.

- Provide project loans to builders so that they can complete housing project in the shortest possible time thus improving their ROI and at the same time reduce the investment period thus reducing the overall cost for the end consumer the main objective of this scheme

The use of these chair style toilets can become the cause of generating constipation, shop for viagra IBS, hemorrhoids, diverticular disease, and other problems. A team appalachianmagazine.com cialis line order of burglars can pretend as a company, and on duty can take your valuables. ED medications contain prescription drugs so they should be taken empty stomach for better results and its performance dips significantly if they are used after a fat rich diet. generic viagra 50mg viagra generika click description Apcalis jelly is an oral dosage similar to sidefacil citrate.

It is envisaged that by the above measures the cost would be 15 to 20% lower than the current market price and by providing long-term loans we would enhance the number of people who can afford to house by 100% in the first three years. The current situation is about half a million people can afford to buy homes and apartments every year.

This will also help us in delivering the promise for 10 million jobs as these houses alone which is an additional 3 million houses over the next five years with each house creating 20 jobs per year means an additional 60 million job-years which means 12 million jobs a year, in unskilled, semi-skilled and skilled category plus another 1 to 1,5 million jobs in related industry and service industry.

This will be doubling the capacity at least of all construction related industry.

This would also mean another one to three hundred thousand jobs in the service industry that is banking, security, maintenance, insurance etc.

This initiative alone would also jumpstart the economy as it will prove to be the biggest growth engine for the economy. The contribution to the country’s economy from the housing sector alone, allied industry and services would be 15 trillion Rupees. (If each unit is valued at 3 million rupees on an average). This would mean an addition of more than 8 to 9 trillion rupees over 5 years above the existing contribution.

Foreclosure law implementation and enactment of new laws. Action: Ministry of law and Parliamentary affairs. Time period 3 months from today.

At the same strengthening of the remortgage finance market to be established. Action: State Bank of Pakistan. Time period: Six months

Selecting locations from existing Federal and Private property owners; Responsibility task force Time Period : Ongoing first 100,000 units next 45 days.

Developing Designs for the units; Responsibility task force next 60 days.

Pricing for each unit as per location through builders 120 days.

Launching of the scheme for booking of units 180 days from today.

Completion of first project and handing over of keys or possession of plots within 2yrs. of this date. Responsibility Task Force, NAYA Pakistan Housing Authority and Private Sector Builders

Every year targets given to all the stake holders are as per the table below which are indicative in nature and will be modified on studying the demand data which is collected every year through actual demand surveys and income levels.

How will the scheme work:

All land titles will be verified by the authority, the land will be acquired by the authority, the authority with the help of builders and developers will decide what product is needed for the market on the basis of the data which the authority would have collected and market study.

Secondly, the authority will also ensure that the necessary infrastructure needed for the project is in place before the scheme is launched which means access, water, sewerage, electricity etc.

Builders will compete to provide the best possible price to the end consumer through a reverse auction/ e-auction.

The houses will be given to the end consumers on first come first basis.

The projects will be completed by the builders by their or own funds or through obtaining loans obtained by the builders for the project. These loans will be repaid by the builders with the accrued interest till the date he has handed over the project to the end consumer.

This financing scheme will ensure that the projects are completed in the shortest possible time. The end consumer is saved from the financial cost.

The price of the land would be not paid by the builder the price of the land would be recovered from the end consumers. The title of the land will be transferred to the bank which will transfer the land to the condominium corporation once the loan is repaid.

The end consumers will have to pay only 20% of the unit price during the construction period but before they would have to obtain financing approval for 80% of the amount for loan from a commercial bank. This loan will be repaid by the homeowner over a period of twenty years. The objective is to bring the installment as close as possible to the rent they are currently paying.

Through the above measures, we hope this will help the builder offer apartments which would be at least 15 to 20% lower than the market prices. Thus making the apartments and the twenty percent down payment as high rated collateral for the loan the bank is giving to the end consumer.

Furthermore, for processing the loan application, the banks would consider the clubbed income of direct relatives such as Husband, wife, and children with an income.

To increase the financial resources of the banks the following sources of funds will be considered, pension funds, zakat funds, provident funds, funds at the disposal of insurance companies, EOBI, Social Security institutions etc.

The banks would be allowed to park funds parked in the housing industry with the remortgage companies on the creation of secondary finance market.

Recent Comments